Whether you are launching a new startup, expanding your e-commerce store across state lines, or just trying to make sense of your latest vendor invoices, understanding India’s Goods and Services Tax (GST) is non-negotiable.

Introduced to create “One Nation, One Tax,” GST actually operates as a dual-structure system. Depending on where you and your customer are located, you will need to deal with three main acronyms: CGST, SGST, and IGST.

Applying the wrong tax type can lead to compliance issues, incorrect invoicing, and blocked Input Tax Credit (ITC). Here is your up-to-date, simplified guide to mastering the three components of GST in 2026.

The Golden Rule: Location is Everything

Before diving into the definitions, you must understand the single most important rule of GST: It is a destination-based tax.

The tax you charge depends entirely on two factors:

-

Location of the Supplier: Where your business is registered.

-

Place of Supply: Where the goods are delivered or services are consumed.

Based on these two locations, transactions fall into two categories:

-

Intra-State Supply: Supplier and Buyer are in the same state.

-

Inter-State Supply: Supplier and Buyer are in different states (or it’s an export/import).

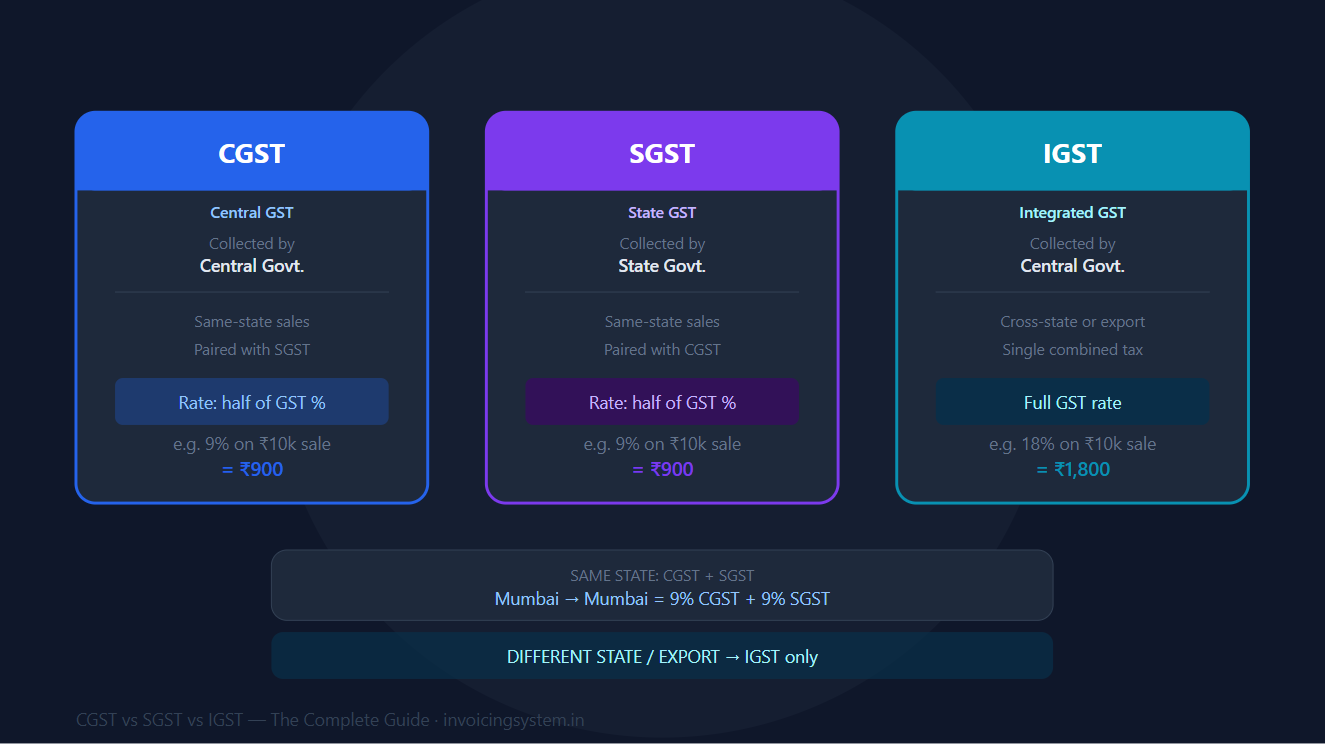

1. What is CGST (Central Goods and Services Tax)?

CGST is the tax collected by the Central Government on intra-state sales (sales happening within the same state).

When you sell a product to a customer within your own state, the total GST rate is split equally into two parts. CGST is the central government’s half of that revenue.

-

Applicability: Intra-state transactions.

-

Revenue goes to: Central Government.

2. What is SGST (State Goods and Services Tax)?

SGST is the tax collected by the State Government on that exact same intra-state sale.

It is the other half of the GST split. (Note: If you operate in a Union Territory like Chandigarh or Lakshadweep, this is replaced by UTGST – Union Territory Goods and Services Tax).

-

Applicability: Intra-state transactions.

-

Revenue goes to: State Government where the sale takes place.

The Intra-State Formula:

Total GST = CGST (50%) + SGST (50%)

3. What is IGST (Integrated Goods and Services Tax)?

IGST is the tax collected by the Central Government on inter-state sales (sales happening between two different states).

Instead of splitting the tax on the invoice, you charge one single combined rate. The Central Government collects the IGST and later distributes the state’s share to the destination state (since GST is a destination-based tax). Imports and exports are also treated as inter-state supplies and attract IGST.

-

Applicability: Inter-state transactions, imports, and exports.

-

Revenue goes to: Central Government (who then apportions the destination state’s share).

Quick Comparison Table

| Feature | Intra-State Sale (Same State) | Inter-State Sale (Different States) |

| Taxes Applied | CGST + SGST | IGST |

| GST Split | 50% Center / 50% State | 100% Collected by Center |

| Example Scenario | Pune (Maharashtra) to Mumbai (Maharashtra) | Pune (Maharashtra) to Bangalore (Karnataka) |

| 18% Tax Breakdown | 9% CGST + 9% SGST | 18% IGST |

Practical Examples: How to Calculate GST

Let’s assume you are a business owner based in Maharashtra selling a batch of electronics worth ₹10,000. The applicable GST rate for electronics is 18%.

Scenario A: Selling to a customer in Nagpur, Maharashtra (Same State)

Because both you and the buyer are in Maharashtra, this is an Intra-State supply.

-

Base Price: ₹10,000

-

CGST (9%): ₹900

-

SGST (9%): ₹900

-

Total Invoice Value: ₹11,800

Scenario B: Selling to a customer in Surat, Gujarat (Different State)

Because the goods are crossing state lines, this is an Inter-State supply.

-

Base Price: ₹10,000

-

IGST (18%): ₹1,800

-

Total Invoice Value: ₹11,800

Notice that the final price for the customer remains exactly the same. The only difference is how the tax is recorded and routed to the government.

Input Tax Credit (ITC) Rules: Setting Off GST

As a registered business, you can claim Input Tax Credit (ITC) on the GST you paid on your purchases to offset the GST you collected on your sales. However, there is a strict hierarchy for how you can set these off against each other in the GST portal:

-

IGST Credit: Must first be used to pay off IGST liability. Any remaining amount can be used to pay off CGST and then SGST in any proportion.

-

CGST Credit: Must first be used to pay off CGST liability. Any remaining amount can be used to pay off IGST. (CGST cannot be used to pay SGST).

-

SGST Credit: Must first be used to pay off SGST liability. Any remaining amount can be used to pay off IGST. (SGST cannot be used to pay CGST).

Conclusion

Mastering CGST, SGST, and IGST is the foundation of smooth financial operations for any Indian business in 2026. By accurately identifying your place of supply and applying the correct taxes, you ensure seamless ITC flow, keep your clients happy, and stay perfectly compliant with the tax authorities.

Need help managing your GST invoices and compliance? Check out our automated invoicing software today!